Savings Interest Calculator

Calculate how much interest you could earn on $1000 in a year. The interest rates shown reflect current 2026 NZ rates for different account types.

Results

How This Compares to Savings Options

Current 2026 NZ rates:

Putting $1000 into a savings account sounds simple, but how much you actually earn in a year depends on one thing: interest rate. It’s not magic. It’s math. And right now, in early 2026, that math looks very different than it did five years ago.

In 2020, you might’ve earned $2 on $1000 in a year. Today? You could earn $40, $50, even $60-if you pick the right account. That’s not a typo. The interest rate landscape has shifted hard, and most people are still using accounts that pay next to nothing.

What’s the average interest rate on savings accounts in 2026?

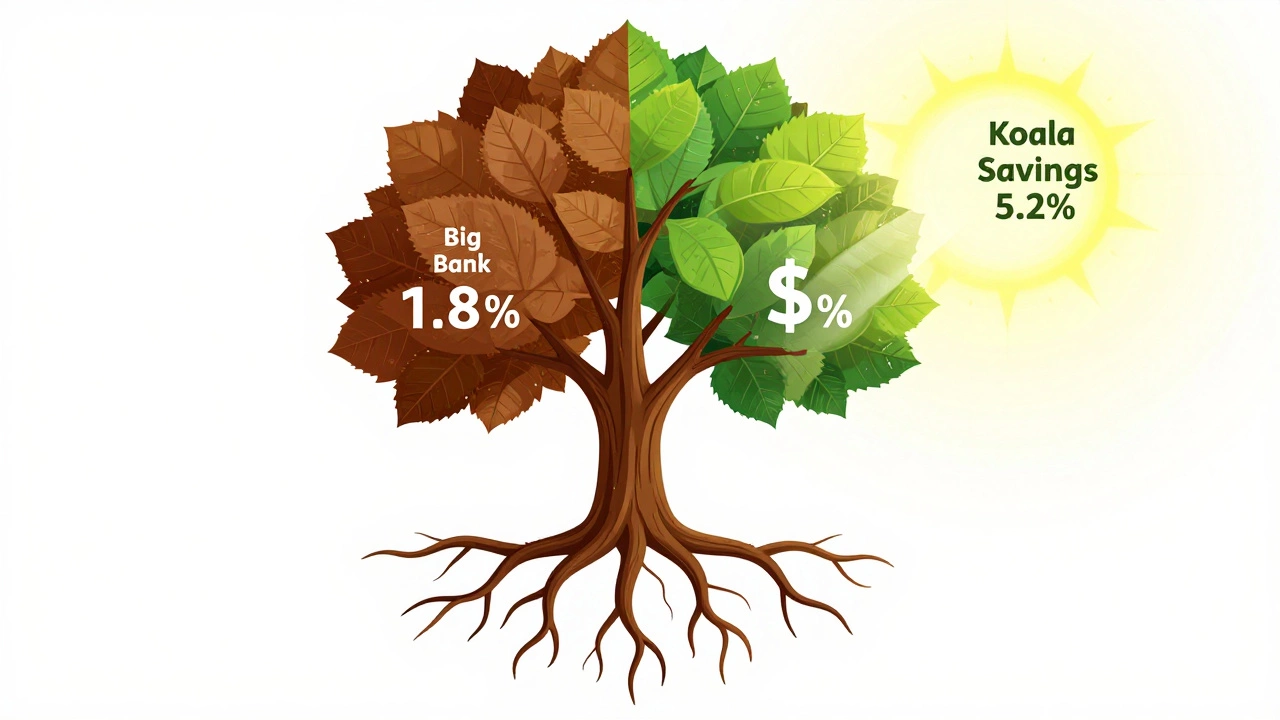

In New Zealand, the big banks-ANZ, ASB, BNZ, and Westpac-still offer standard savings accounts with rates around 1.5% to 2.5%. That means $1000 earns between $15 and $25 in a year. Sounds underwhelming? It is. But here’s the catch: those aren’t the best options anymore.

Online-only banks and fintech platforms have stepped in. Think of them as the discount stores of banking. They don’t have branches, so they cut costs. That lets them pay you more. Accounts like Koala Savings, Spaceship Money, and Rabobank’s online savings account are offering 4.7% to 5.3% right now. That’s not a promo. That’s their standard rate.

So if you put $1000 into one of those, you’d earn about $47 to $53 in interest over 12 months. No tricks. No fine print. Just a better rate.

How compounding changes the game

Interest isn’t always paid once a year. Most accounts pay monthly. That’s where compounding comes in. It doesn’t sound like much, but it adds up.

Let’s say you put $1000 into an account that pays 5% annually, compounded monthly. Each month, you get 0.4167% of your balance added. So in the first month, you earn $4.17. The next month, you earn a little more-because your new balance is $1004.17. By the end of the year, you won’t earn exactly $50. You’ll earn $51.16.

That extra $1.16? It’s the power of compounding. It’s small, but over time, it stacks. If you leave $1000 in that account for five years, you’ll earn nearly $280 in interest-not $250. That’s $30 extra just because the bank compounds monthly.

What’s the difference between a regular savings account and a high-yield one?

Regular savings accounts are what you get when you walk into a bank branch. They’re easy to open, linked to your everyday account, and come with no surprises. But they’re designed to keep your money safe, not grow it.

High-yield savings accounts (HYSA) are built for growth. They usually require you to open an account online, and some have rules: minimum deposits, no withdrawals for 30 days, or limits on how many transfers you can make per month. But they pay 3 to 5 times more than your local bank.

Here’s a quick comparison:

| Account Type | Annual Interest Rate | Interest Earned in 1 Year |

|---|---|---|

| Big Bank Standard Savings | 1.8% | $18 |

| Online Savings Account (e.g., Koala) | 5.2% | $52 |

| Term Deposit (12-month) | 4.9% | $49 |

| Cash Management Account | 4.6% | $46 |

| Supermarket Savings Account | 3.1% | $31 |

The gap isn’t just numbers. It’s real money. $52 instead of $18? That’s enough to cover a full tank of petrol, a few groceries, or even a weekend away. It’s not life-changing-but it’s a step toward building habits that compound over time.

What about inflation?

You’ve probably heard that inflation eats away at your money. In early 2026, New Zealand’s inflation rate is hovering around 2.8%. That means if your savings account pays 1.8%, you’re actually losing purchasing power. Your $1000 buys less next year than it did this year.

But if you’re earning 5.2%, you’re not just keeping up-you’re ahead. You’re gaining real value. That’s why choosing a high-yield account isn’t just about being smart with money. It’s about protecting it.

Can you get more than 5%?

Yes, but with trade-offs. Some accounts offer 6% or even 7% for a limited time-usually for new customers. But those are often temporary. After 3 or 6 months, the rate drops back to 3% or 4%. That’s a bait-and-switch. Don’t fall for it.

Others require you to lock your money away for 12 months (term deposits). That’s fine if you don’t need the cash. But if you need flexibility-say, for emergencies or unexpected bills-you’ll pay a penalty to withdraw early. That penalty can wipe out your interest.

So if you want to earn more than 5%, ask yourself: Do I need access to this money? If yes, stick with a high-yield savings account that pays 5% and lets you withdraw anytime. If no, a 12-month term deposit at 4.9% might be better.

What should you do with 00 right now?

Don’t leave it in your everyday bank account. Seriously. That’s the worst place for it.

Here’s what to do instead:

- Compare rates on Interest.co.nz or Sorted.org.nz. Both are government-backed and updated daily.

- Open an account with a fintech provider like Koala or Spaceship. You can do it in 5 minutes on your phone.

- Transfer your $1000. No minimums. No fees.

- Set up an automatic transfer of $50 or $100 every month. Even small amounts add up.

By the end of the year, you’ll have $1050 plus whatever you added. That’s not just interest. That’s momentum.

Why does this matter beyond $1000?

Because habits matter more than numbers. If you learn how to earn $50 on $1000 this year, you’ll start thinking differently about your money. You’ll look at your other accounts. You’ll ask, "Why am I earning so little?" You’ll move your emergency fund. You’ll start a second savings goal. You’ll begin to see your money as something that works for you-not just something you keep.

That’s the real win. Not the $50. The mindset shift.