What Is the Maximum Equity Release You Can Take Out?

Discover how much equity you can actually release from your home in 2026. Learn the factors setting your limit, including age, property type, and loan options.

If you own a home and need extra cash, equity release might be on your radar. It lets you turn part of your house value into a lump sum or regular payments without moving out. The idea sounds straightforward, but the details matter – especially the type of plan, how interest is charged, and what you’ll owe back.

There are two main flavors: a lifetime mortgage and a home reversion deal. With a lifetime mortgage, you borrow against your home and the loan plus interest rolls up over time. You don’t make monthly repayments; the balance is usually settled when you die or move into long‑term care. A home reversion plan means you sell a share of your property (often 25‑50%) to a specialist and keep living there rent‑free. You’ll get a smaller cash amount up front, but you won’t owe interest.

Interest rates on lifetime mortgages are higher than standard mortgages because the loan is unsecured until death. Some providers let you choose a fixed rate, while others offer a variable rate that can change with the market. The interest compounds, so the debt grows faster than a regular loan. That’s why it’s crucial to run the numbers and see how much of your home will be left for heirs.

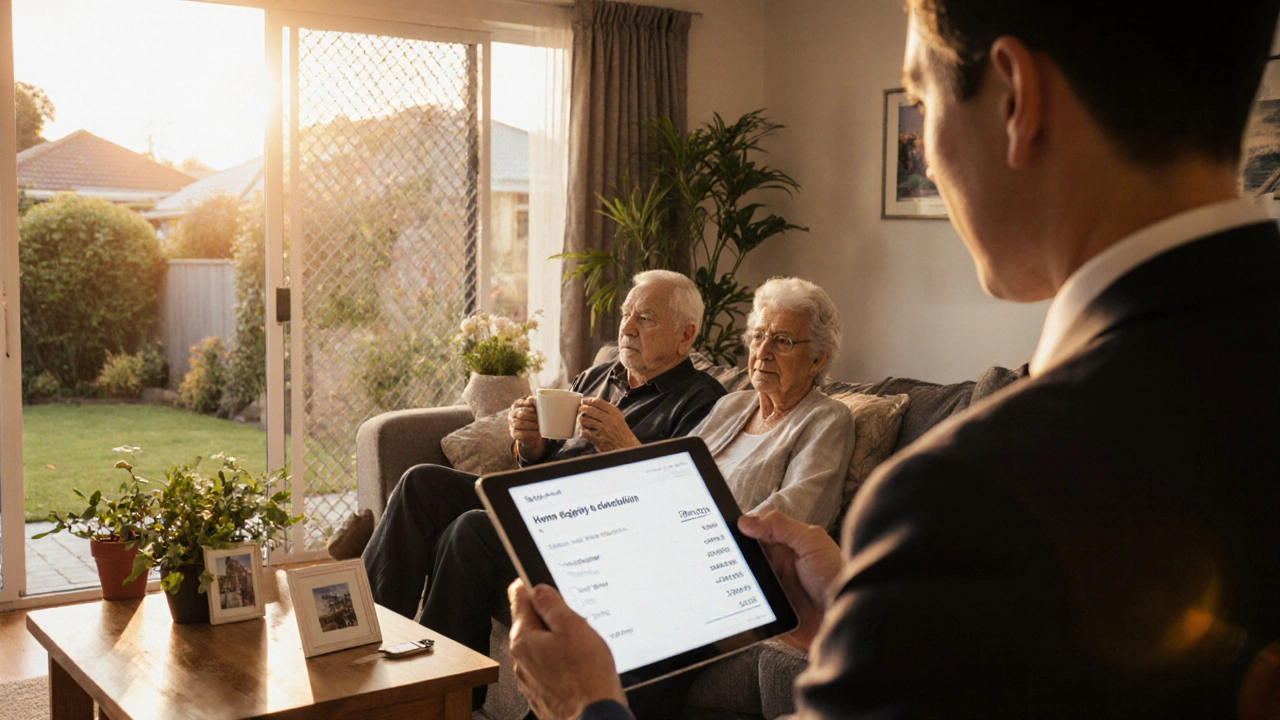

First, ask yourself why you need the money. If it’s for a one‑off expense like home repairs, a lump‑sum lifetime mortgage might fit. If you want a steady income stream, some plans let you take monthly payments instead of a big payout. Second, consider your health and life expectancy. The longer you live, the more interest accrues, eating into the equity you leave behind.

Third, compare providers. Look at the interest rate, any early repayment charges, and the level of cash you get for the same percentage of equity. Our article “How Much Do You Repay on Equity Release? All You Need to Know in 2025” breaks down the maths with real‑world examples, so you can see the impact of different rates.

Finally, talk to a qualified adviser. Equity release is a big decision and can affect your eligibility for state benefits. A specialist can run a free assessment, check if you qualify for the government’s equity release guarantee, and help you pick the plan that matches your goals.

Remember, equity release isn’t free money – it’s a loan that sits on your home until the end of the term. Make sure you understand the total amount you’ll owe, how it will affect your estate, and whether you’re comfortable with the interest build‑up. With the right research and advice, you can unlock cash without selling your house outright.

Discover how much equity you can actually release from your home in 2026. Learn the factors setting your limit, including age, property type, and loan options.

Find out exactly how much equity you can release from your home in New Zealand based on your age, property value, and health. Learn the real limits, hidden costs, and smart alternatives before you commit.

How much can you release from your home? Learn the real maximums, what affects them, UK vs NZ differences, quick formulas, examples, and pitfalls to avoid.

Curious if equity release means you’ll have monthly payments? Get the facts, including how various products work and what to expect financially.

Learn what 'guaranteed' really means for equity release – the must-know facts, risks, and protections homeowners get when tapping property value.

Looking for the cheapest way to take equity out of your home? Learn which method fits your situation best, how fees add up, and what to avoid in 2025.

Ever wondered what actually happens to your mortgage when you release equity from your home? This article explains how releasing equity affects your existing mortgage, what new costs can show up, and how your homeownership could change. Get tips for spotting common lender terms, protecting your home's value, and avoiding financial surprises. Find out which equity release options make sense if you just want cash or if you still need flexibility in the future. Find real talk on making smart moves with your mortgage and home equity.

Looking for cash but don't want the hassle of refinancing your home? There's good news—several ways let you tap your home's equity without starting a new mortgage. This article breaks down home equity loans, HELOCs, and shared equity agreements, and explains the pros and cons of each. You'll also get tips to avoid common pitfalls. Say goodbye to endless paperwork and rate shopping—here’s how to unlock your home's value on your own terms.

Wondering when you can pull equity out of your home? This article breaks down the exact point homeowners can access their equity, why timing matters, and what lenders really look for. Get practical tips to boost your home's value and avoid common missteps. Learn how life situations and the fine print play into making a smart move.

Understanding the minimum credit score required for an equity loan can be crucial when you're looking to unlock the value of your home. While it's generally accepted that a higher credit score improves your chances, knowing the specific requirements can clear up any uncertainties. This article explores the credit score benchmarks, factors influencing lender decisions, and practical tips to improve your score. Essential for anyone considering tapping into their home equity. Discover how to navigate this financial journey effectively.

Navigating the world of equity release can be complex, especially with numerous companies offering diverse options. This article explores key players in the equity release market, offering insights into their strengths and benefits. We'll also highlight important considerations to keep in mind when selecting a company. Whether you're looking to unlock the value of your property or plan for financial freedom, understanding these companies can guide you in making informed decisions.

Choosing the best equity release provider is a crucial decision for those looking to unlock home value in 2025. With providers offering various options, it's essential to understand the market, consider all features, and know what suits your individual needs. Interest rates, customer service, and flexibility are key factors. We'll dive into expert tips and insights to guide you through the process and help you make an informed decision.