Equity Release Options: What They Are and How They Work in the UK

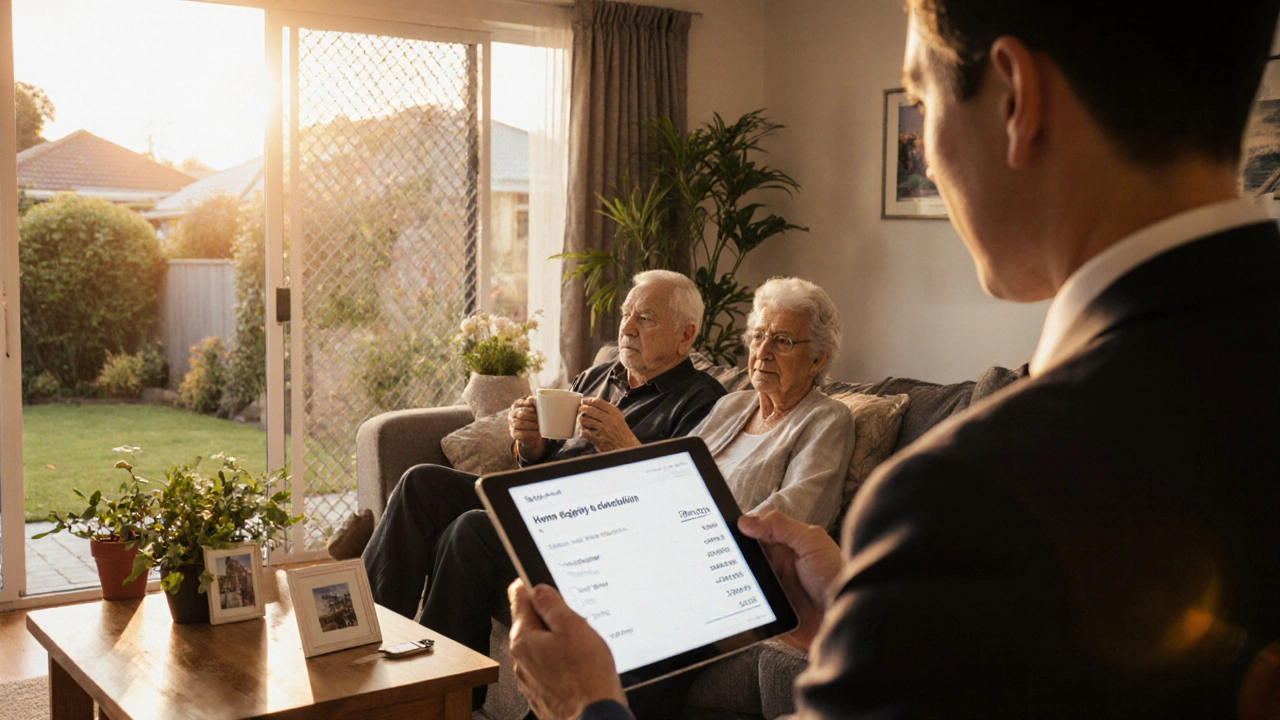

When you own a home but need extra cash in retirement, equity release options, ways to access the value tied up in your home without selling it outright. Also known as home equity release, these tools let you turn your property into income or a lump sum while still living there. This isn’t about downsizing or moving—it’s about unlocking what’s already yours.

There are two main types of equity release: lifetime mortgages, loans secured against your home that you don’t repay until you die or move into long-term care, and home reversion, schemes where you sell part or all of your home in exchange for cash, keeping the right to live there rent-free. Both are designed for people over 55, and both come with rules about interest, repayment, and what happens to your estate. A lifetime mortgage lets you borrow a percentage of your home’s value—often up to 60%—and interest rolls up over time. A home reversion plan gives you a lump sum or regular payments, but you give up ownership. Neither affects your state pension, but they can reduce what you leave to your family.

These options aren’t right for everyone. If you’re planning to move soon, or if you want to leave your home to your kids, you’ll need to think carefully. But for many older homeowners in the UK, equity release is the only way to cover medical bills, home repairs, or even a holiday without dipping into savings or taking on a new loan. The Financial Conduct Authority (FCA) requires all providers to offer free advice, and you must use a solicitor to protect your interests. That’s not bureaucracy—it’s a safety net.

What you’ll find below are real posts that break down how these plans actually work, what they cost, how they compare to other retirement income tools, and what happens when things change—like if you need care later, or if property values drop. No fluff. No sales pitches. Just clear, practical info from people who’ve been there.