KiwiSaver Growth Calculator

See how your retirement savings could grow over time. This calculator uses a 6% annual growth rate (historical average for balanced funds) to estimate your retirement balance.

When you hear the word pension plan, you might think of old-school company pensions or government cheques. But in 2026, a pension plan is something far more personal - and far more important. It’s not just something your employer gives you. It’s your own long-term savings system, designed to turn your daily work into reliable income when you stop working. And if you’re in New Zealand, you’re already part of one - whether you realize it or not.

What exactly is a pension plan?

A pension plan is a structured way to save money during your working life so you can live comfortably after you retire. It’s not a single product. It’s a system. Some are run by your employer. Some are run by the government. Some you set up yourself. But they all share the same goal: take a little bit of your income now, invest it over time, and turn it into regular payments when you’re no longer earning a salary.

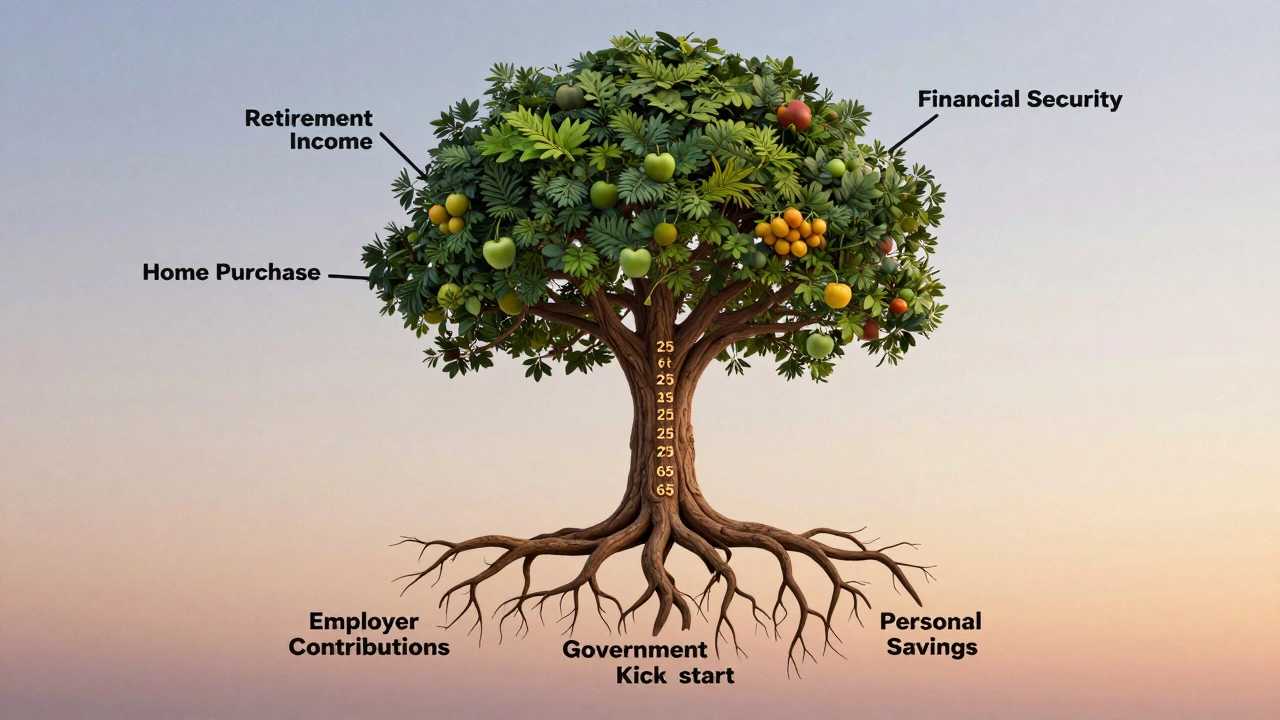

In New Zealand, the most common form is KiwiSaver. It’s not called a pension plan officially, but it functions exactly like one. Every time you get paid, a portion of your salary goes into your KiwiSaver account - usually 3%, 4%, or 8% - and your employer adds at least 3%. The government throws in a small annual kickstart too. That money gets invested in funds you choose, and over 30 or 40 years, it grows.

Outside of KiwiSaver, some people still have traditional pension plans, especially in the public sector or large companies. These are often called defined benefit plans. That means your retirement income is calculated based on your salary and how long you worked - not on how much you saved. For example, you might get 60% of your final salary each year after retirement. These are rare now, but they still exist.

How does a pension plan actually work?

Think of it like a long game of compound interest. Let’s say you start contributing $100 a week to your pension plan at age 25. That’s $5,200 a year. Your employer adds another $5,200. The government adds $520. You’re putting in $10,920 a year. Now imagine that money grows at 6% a year - not crazy, that’s the historical average for balanced funds.

By the time you’re 65, that’s over $1.1 million. Not because you saved $1.1 million. You saved about $436,800 total. The rest? Growth. That’s the power of time.

Most pension plans work like this:

- You contribute a percentage of your pay (pre-tax or after-tax, depending on the plan).

- Your employer contributes too - sometimes matching yours, sometimes not.

- The money is invested in a mix of shares, bonds, property, and cash.

- Over decades, those investments grow.

- At retirement, you start drawing money out - either as regular payments, a lump sum, or a mix of both.

The key? Start early. Even small amounts add up. If you wait until 40 to start, you’ll need to save nearly double what someone who started at 25 saves - just to get the same result.

Types of pension plans

Not all pension plans are the same. Here are the three main types you’re likely to encounter:

Defined Contribution Plans

This is what most people have today. Your retirement income depends on how much you and your employer put in, and how well the investments grow. KiwiSaver is a defined contribution plan. So are 401(k)s in the U.S. and workplace pensions in the UK. You get to choose your investment options - conservative, balanced, growth - and your final amount depends on your choices.

Defined Benefit Plans

These are the old-school pensions. Your retirement income is guaranteed based on your salary and years of service. For example: “You’ll get 2% of your final salary for each year you worked.” So if you worked 30 years and your final salary was $80,000, you’d get $48,000 a year for life. These are rare now because they’re expensive for employers to fund. You’ll mostly find them in government jobs, police, firefighters, or some large unions.

Individual Retirement Accounts (IRAs)

In the U.S., IRAs are personal pension plans you set up yourself. In New Zealand, KiwiSaver fills that role. But if you’re self-employed or work freelance, you can open a personal pension account - sometimes called a self-directed retirement fund. These give you full control over where your money goes, but also full responsibility for managing it.

How KiwiSaver fits into the picture

If you’re working in New Zealand, you’re probably in KiwiSaver. It’s automatic. You can’t opt out unless you’re self-employed or over 65. But you can choose how much to contribute - 3%, 4%, 6%, or 8%. The government adds $521 a year if you contribute at least $1,042. Your employer must contribute 3% of your gross pay (unless you’re on a savings suspension or contribution holiday).

Here’s what most people don’t realize: KiwiSaver isn’t just for retirement. You can use it to buy your first home after three years. That’s a huge advantage. But if you don’t touch it, it keeps growing. And if you start at 18 and save 8% of $50,000 a year, you could have over $1 million by 65.

What happens when you retire?

At retirement, you don’t get a monthly cheque from the government unless you’re on the New Zealand Superannuation - which is a separate state pension. Your pension plan money is yours to access. You have options:

- Withdraw it as a lump sum (but watch out for tax implications).

- Buy an annuity - a product that pays you regular income for life.

- Leave it invested and withdraw small amounts each year (this is what most people do).

- Use it to pay off debt or fund lifestyle changes.

The smartest move? Don’t cash out everything at once. If you do, you risk running out of money. Instead, treat it like a second salary. Withdraw 4% to 5% a year - adjusted for inflation - and let the rest keep growing.

Common mistakes people make

Even people who understand pension plans mess up. Here are the top three mistakes:

- Starting too late. Waiting until 35 or 40 means you need to save way more each month. It’s harder. It’s stressful. And it rarely works.

- Choosing the wrong fund. If you’re 25 and in a cash fund, you’re missing out on growth. If you’re 62 and in a growth fund, you’re risking big losses right before retirement.

- Ignoring employer contributions. If your employer matches 3%, that’s free money. Not taking it is like leaving $1,500 a year on the table.

Also, don’t forget to check your fund’s fees. A 1.5% annual fee might sound small, but over 40 years, it can cut your final balance by 30% or more.

What if you’re self-employed?

If you don’t have an employer, you still need a pension plan. KiwiSaver still works - you just have to make all the contributions yourself. Set up automatic transfers. Even $50 a week adds up. Or open a personal retirement account with a provider like SuperLife, Aon, or SmartDollar. The rules are the same: invest early, invest consistently, and don’t touch it.

Is a pension plan the same as superannuation?

In New Zealand, yes - sort of. “Superannuation” usually refers to the government’s age-based payment - the $600 a fortnight most people get at 67. But in other countries like Australia, “super” means the same thing as KiwiSaver: a workplace retirement savings plan. So when people say “super,” they might mean different things depending on where they’re from. In NZ, stick to “KiwiSaver” for your savings plan, and “NZ Super” for the government payment.

What should you do next?

If you’re not sure where you stand:

- Log in to your KiwiSaver account. Check your balance. Check your fund type. Check your fees.

- Make sure you’re contributing at least 4% - that’s the sweet spot for most people.

- Choose a fund that matches your age and risk tolerance. If you’re under 35, go growth. If you’re over 55, go balanced or conservative.

- Set a reminder to review your plan every year.

You don’t need to be a finance expert. You just need to be consistent. The system works. But only if you show up.

Final thought

A pension plan isn’t about getting rich. It’s about not running out of money. It’s about being able to pay your bills, take a holiday, or help your grandkids without asking for help. It’s about dignity in retirement. And it’s not something you do once. It’s something you do every pay day - for decades. Start now. Even if it’s small. Because tomorrow’s you will thank today’s you.

Is a pension plan the same as KiwiSaver?

In New Zealand, KiwiSaver is the main type of pension plan. It’s a government-backed, employer-supported retirement savings scheme. While the word "pension" is sometimes used loosely, KiwiSaver is technically a defined contribution plan - not a traditional pension. But functionally, it serves the same purpose: saving for retirement.

Can I access my pension plan before retirement?

In KiwiSaver, you can access funds early only under specific conditions: buying your first home, serious financial hardship, permanent emigration, or serious illness. Otherwise, you must wait until you’re 65. Other pension plans may have different rules, but early access usually comes with penalties or taxes.

How much should I contribute to my pension plan?

Aim for at least 10% of your gross income - that includes your contribution and your employer’s. In KiwiSaver, that means contributing 6% or 8% yourself. The 3% from your employer brings you to 9%-11%. That’s the sweet spot for most people to retire comfortably. If you can afford more, do it.

What happens to my pension plan if I change jobs?

Nothing. Your KiwiSaver account stays with you. Your new employer will automatically continue contributions at the same rate unless you change it. You don’t need to open a new account. Just make sure your new employer has your KiwiSaver details. If you’re unsure, check your Inland Revenue account.

Do I still get NZ Super if I have a pension plan?

Yes. NZ Super is a government-funded pension paid to most people over 67, regardless of how much you’ve saved. Your KiwiSaver or other pension plan is separate. You get both. NZ Super is not means-tested - so even if you’re rich, you still get it. But it’s not designed to be your only income. That’s why your pension plan matters.

Can I have more than one pension plan?

You can only have one KiwiSaver account, but you can have multiple retirement savings accounts - like a personal investment account or a self-managed super fund (if you’re overseas). Just be careful: too many accounts can make it hard to track your total savings. Consolidating into one or two is usually smarter.