Homeowners Insurance 80% Rule Calculator

Calculate whether your dwelling coverage meets the 80% coinsurance requirement and see exactly how much you'd receive on a claim.

How the 80% Rule Works:

- Calculate required coverage: Replacement Cost × Coinsurance %

- Compare your actual coverage to the required amount

- If below threshold, penalty applies proportionally

- Formula: (Coverage Carried / Required) × Loss = Payout

Example Scenario:

- Replacement Cost: $500,000

- Required (80%): $400,000

- Your Coverage: $300,000

- Status: Penalty Applies

Calculation Results

Scenario Comparison

| Scenario | Coverage Level | Payout | Out-of-Pocket |

|---|

You just bought a beautiful Victorian home in a historic district. You pay your premiums on time. You think you’re fully covered. Then, a fire damages half your roof and gutters. You file a claim, expecting your insurance to cover the full repair cost minus your deductible. Instead, they send you a check for significantly less than you need. The contractor looks at you with pity. The adjuster points to a clause you never read: the 80% rule is a standard provision in homeowners insurance policies that requires policyholders to insure their home for at least 80% of its replacement cost to receive full payment on partial losses.

This isn’t a scam. It’s not even particularly rare. It’s the most misunderstood concept in property insurance. If you don’t understand how this rule works, you might be paying for coverage that doesn’t actually protect you when disaster strikes.

The Core Problem: Underinsurance Without Knowing It

Most people buy homeowners insurance based on what they paid for the house or what their bank requires. That’s a mistake. Banks care about the land value and the loan amount. Insurers care about how much it costs to rebuild the structure from scratch if it burns down.

Here’s the trap: If your home would cost $500,000 to rebuild today, but you only carry $300,000 in dwelling coverage, you are underinsured. In fact, $300,000 is only 60% of the replacement cost. Because you fell below the 80% threshold ($400,000), you trigger the coinsurance penalty is a financial reduction applied to insurance claims when the policyholder fails to meet the minimum required coverage percentage relative to the home's replacement value.

When this happens, the insurer argues that you were trying to save money by buying less coverage, so they will share the risk with you on every claim-not just total losses, but even small ones like a burst pipe or a fallen tree branch.

How the Math Actually Works

Let’s break down the formula insurers use. It looks complicated, but it’s straightforward once you see the numbers.

| Factor | Value |

|---|---|

| Actual Replacement Cost of Home | $500,000 |

| Required Coverage (80%) | $400,000 |

| Your Actual Dwelling Coverage | $300,000 |

| Claim Amount (Damage) | $100,000 |

| Deductible | $1,000 |

Without the 80% rule, you’d expect to get $99,000 ($100,000 damage minus $1,000 deductible). But because you only carried $300,000 against a required $400,000, the insurer calculates your share of the loss proportionally.

The formula is: (Amount of Insurance Carried / Amount of Insurance Required) × Loss Amount = Payout

In our example: ($300,000 / $400,000) × $100,000 = $75,000.

After subtracting your $1,000 deductible, you receive $74,000. You are now responsible for the remaining $25,000 out of pocket. For a partial loss, you’ve just become your own insurer for a quarter of the bill.

Why Do Insurers Use This Rule?

It seems harsh, but there’s logic behind it. Insurance is a pool of shared risk. When you buy a policy, you’re agreeing to contribute enough premium to keep the pool solvent. If everyone could buy tiny amounts of coverage while still receiving full payouts for partial losses, the system would collapse. People would game the system by carrying minimal limits.

The 80% threshold exists to ensure that policyholders have a significant financial stake in protecting their property. It prevents adverse selection, where only high-risk properties get insured with low limits. By requiring 80% coverage, insurers ensure that most homeowners are adequately protected against catastrophic events, which keeps premiums stable for everyone.

However, the burden falls on you, the policyholder, to know your home’s true replacement cost. Many people assume their policy automatically adjusts for inflation or construction cost increases. It usually doesn’t, unless you’ve specifically purchased an endorsement for it.

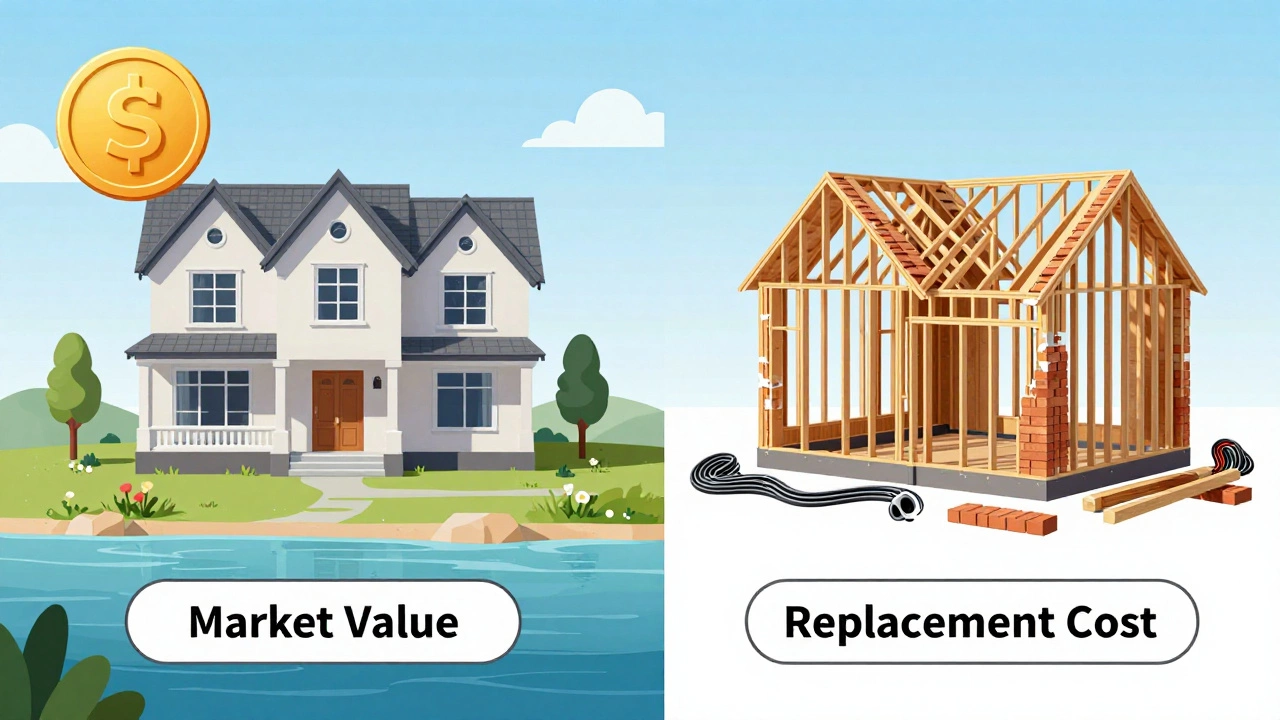

Replacement Cost vs. Market Value: A Critical Distinction

This is where most people go wrong. Your home’s market value includes the price of the land, location desirability, school districts, and current real estate trends. Your home’s replacement cost includes only the materials and labor needed to rebuild the structure itself.

If your home sits on a valuable lot in Auckland’s waterfront area, the land might account for 60% of the sale price. But if the house burns down, the insurer doesn’t pay you for the land-they already own it through your mortgage equity. They only pay to rebuild the bricks, mortar, wiring, plumbing, and roofing.

To find your true replacement cost, you can:

- Use online estimators provided by insurance companies (though these can be inaccurate).

- Hire a professional appraiser who specializes in replacement cost valuation.

- Contact local contractors for quotes on similar reconstruction projects.

Construction costs vary wildly by region. In areas prone to earthquakes or hurricanes, building codes require more expensive materials and engineering. These factors must be reflected in your coverage limit.

Guaranteed Replacement Cost: The Exception

Some policies offer a feature called Guaranteed Replacement Cost is an optional endorsement that removes the 80% rule limitation and promises to pay the full cost of rebuilding your home regardless of the policy limit or current construction prices. With this endorsement, the 80% rule disappears. Even if construction costs skyrocket after a major disaster, the insurer covers the difference.

This sounds perfect, right? There are caveats:

- Higher Premiums: This coverage costs more upfront.

- Reasonable Limits: You still need to start with a reasonable estimate of replacement cost. Insurers won’t guarantee unlimited funds if you started with a grossly underestimated base amount.

- Like-for-Like Repairs: Most guaranteed replacement policies require you to rebuild with similar materials and design. Upgrading to marble countertops during repairs may not be covered.

If you live in an area with volatile construction markets or unique architectural features, this endorsement can be worth the extra cost. Otherwise, sticking to the standard 80% rule with accurate valuation is sufficient.

Other Structures and Personal Property

The 80% rule typically applies only to the main dwelling (Coverage A). However, other parts of your policy have their own rules.

Coverage B (Other Structures) usually provides automatic coverage equal to 10% of your dwelling limit. If your garage or detached shed burns down, this separate limit applies. The 80% rule generally doesn’t penalize you here, but you can still run out of money if you have multiple large outbuildings.

Coverage C (Personal Property) often has sub-limits for specific items like jewelry, art, or electronics. These categories operate independently of the 80% rule. If you lose a $5,000 camera and your policy caps cameras at $1,500, you’ll only get $1,500. No proportional penalty applies-it’s just a hard cap.

Understanding these distinctions helps you allocate your budget wisely. Don’t overspend on dwelling coverage if your personal property needs aren’t addressed via riders or floaters.

How to Avoid the Trap

Avoiding the 80% rule penalty comes down to proactive management. Here’s what you should do:

- Review Annually: Construction costs rise every year. Check your dwelling coverage limit annually before renewing your policy.

- Track Renovations: Did you add a sunroom? Upgrade your kitchen? Increase your square footage? Notify your insurer immediately. These changes increase your replacement cost.

- Ask for a Re-evaluation: If you haven’t had your home valued in three years, ask your agent to order a new replacement cost estimate. Many insurers offer this service for free.

- Consider Inflation Guard: Some policies include an endorsement that automatically adjusts your coverage based on local construction cost indices. This is cheaper than guaranteed replacement cost and provides peace of mind.

Don’t rely on your mortgage statement. Lenders require hazard insurance, but they don’t verify that the amount matches current replacement costs. They only care that the loan is secured.

Common Misconceptions

“I’m over-insured, so I’m safe.” Actually, being slightly over-insured is fine. If your replacement cost is $500,000 and you carry $600,000, you won’t get paid more than $500,000 for a total loss. But you also won’t face penalties for partial losses. The excess premium is wasted money, but the protection is solid.

“The 80% rule applies to my entire policy.” No. It applies specifically to the dwelling coverage (Coverage A). Other sections have different structures and limitations.

“My insurer will tell me if I’m underinsured.” They might, but they aren’t legally obligated to warn you before a claim. Their duty is to explain the terms when you sign up. After that, maintaining adequate coverage is your responsibility.

Does the 80% rule apply to renters insurance?

No. Renters insurance covers your personal belongings and liability, not the structure itself. Since you don’t own the building, there is no replacement cost for the dwelling to calculate. However, some renters policies may have similar coinsurance clauses for high-value personal property, though this is rare.

What happens if my home is completely destroyed?

In the case of a total loss, the 80% rule penalty usually does not apply. You will receive up to your policy limit. If your limit is lower than the actual replacement cost, you simply receive the limit amount. The penalty primarily affects partial losses, where the insurer reduces the payout proportionally based on your underinsurance level.

Can I negotiate the 80% rule with my insurer?

You cannot change the 80% threshold itself-it’s a standard industry practice. However, you can choose a policy with Guaranteed Replacement Cost or Extended Replacement Cost endorsements, which effectively bypass the rule. You can also shop around for insurers who offer more flexible valuation methods or higher default percentages.

How often should I update my dwelling coverage?

At least once a year, preferably at renewal time. Additionally, update it immediately after any major renovation, addition, or significant change in local construction costs. If your area experiences rapid inflation in building materials, consider mid-year reviews.

Is the 80% rule the same in every state?

While the concept is widespread, specific regulations vary by jurisdiction. Some states may mandate different minimum percentages or require insurers to provide clearer disclosures. Always check your local insurance department guidelines and read your specific policy wording, as contracts can differ between providers.