New Zealand Mortgage Rate Calculator

Calculate Your Monthly Payments

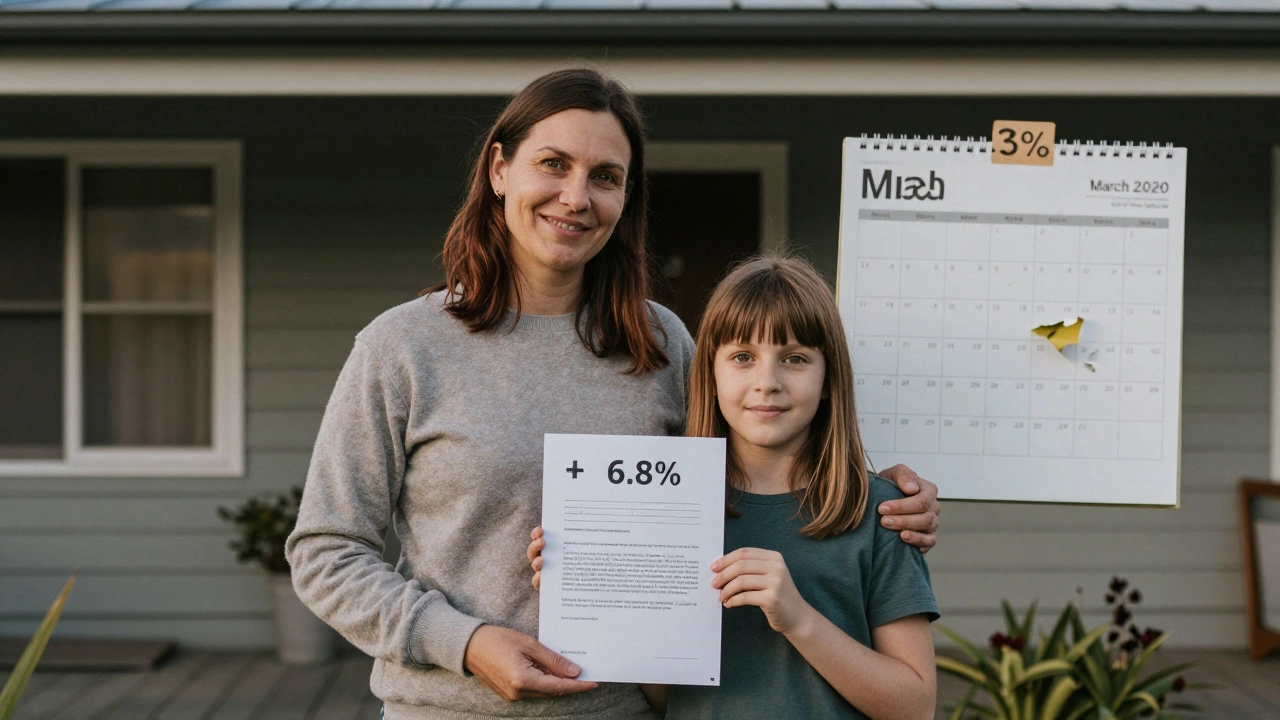

Back in 2020 and 2021, getting a mortgage at 3% felt almost normal. People were locking in rates that seemed like a steal. Now, in early 2026, the average fixed-rate mortgage in New Zealand sits around 6.8%. That’s nearly double. So the question on everyone’s mind: Will mortgage rates ever be 3% again?

What made 3% mortgages possible?

The last time rates dipped below 4% was during the pandemic. Central banks around the world slashed interest rates to near zero to keep economies from collapsing. The Reserve Bank of New Zealand dropped the Official Cash Rate to 0.25% in March 2020. Banks passed those savings on to borrowers. At the same time, housing demand exploded. People moved out of cities, remote work took off, and savings piled up. Lenders were desperate to lend. Rates didn’t just drop - they plummeted.

But that was a perfect storm. Not a new normal. When inflation hit 7.3% in late 2022, the RBNZ had no choice but to reverse course. They raised the OCR to 5.5% by late 2023. Mortgage rates followed, climbing steadily. By 2025, lenders were pricing in long-term inflation risks, not pandemic-era panic.

Could rates go back to 3%? The economic reality

For mortgage rates to fall back to 3%, a few big things would have to happen - all at once.

- The Reserve Bank would need to cut the Official Cash Rate to around 1% or lower.

- Inflation would have to fall and stay below 1.5% for at least two years.

- The global economy would need to enter a prolonged period of low growth or deflation.

- House prices would need to drop significantly - by 20% or more - to justify such low rates.

None of that is on the horizon. In fact, New Zealand’s inflation is hovering around 2.1% in early 2026 - close to the RBNZ’s target range. The economy is stabilizing. Wages are rising. Housing demand is creeping back, especially with immigration levels returning to pre-pandemic numbers.

Even if the RBNZ starts cutting rates in late 2026 or 2027, they’re unlikely to go below 2%. That would put mortgage rates around 4.5% to 5%, not 3%. A 3% rate would require a full-blown economic crisis - not a gentle correction.

What history tells us

Looking at New Zealand’s mortgage rate history since the 1980s, 3% was almost unheard of. Before the pandemic, the lowest average fixed rate recorded was 4.1% in 2016. Before that? Rates were in the 6-8% range for most of the 2000s. Even during the 2008 financial crisis, rates didn’t dip below 5% for long.

The 3% era was an anomaly. It was the result of extraordinary monetary policy, not a sign of how things “should” be. Think of it like a once-in-a-lifetime sale at a store. Just because you got something for half price once doesn’t mean it’ll ever be that cheap again.

Compare that to countries like Japan or Switzerland, where rates have stayed near zero for decades. New Zealand’s economy doesn’t operate like theirs. We don’t have massive government debt overhangs or aging populations crushing demand. We’re still growing. We still need to borrow. That keeps rates higher.

What’s realistic for the next five years?

Most economists expect mortgage rates to drift down slowly over the next few years - but not all the way to 3%. Here’s what’s likely:

- 2026-2027: Rates hold steady or dip slightly to 6.2%-6.5% as inflation cools further.

- 2028-2029: If the RBNZ cuts OCR to 2.5%, fixed rates could reach 5.5%-5.8%.

- 2030: The lowest we might realistically see is 5% - and even that would require a major global slowdown.

That’s still 2 full percentage points above 3%. And remember: 5% is still a very low rate by historical standards. For most homeowners, it’s manageable.

Why chasing 3% is a trap

Many people are waiting to buy a home until rates drop back to 3%. That’s a dangerous mindset. It’s like waiting for the lottery to win before you buy a ticket. The odds are stacked against you.

Here’s what you risk:

- Price appreciation: If rates dip even slightly, demand spikes. House prices jump. You might wait for a 3% rate, but end up paying $150,000 more for the same house.

- Opportunity cost: Renting while you wait means you’re not building equity. Over five years, that’s tens of thousands lost.

- Rate surprises: If inflation picks up again - say, due to supply chain issues or global conflict - rates could climb higher again. You’d be stuck waiting longer.

There’s no guarantee 3% will ever return. But there’s a high chance that waiting for it will cost you more than paying 5% today.

What to do instead

If you’re thinking about buying or refinancing, stop asking if rates will hit 3%. Ask these instead:

- Can I afford a mortgage at 5.5% for the next 10 years?

- Do I have a 20% deposit and a stable income?

- Is this home a place I want to live in for at least 5 years?

- Can I handle a 1% rate increase without panic?

Fixing your rate for 3-5 years right now might feel expensive, but it gives you certainty. In a world of uncertainty, that’s worth more than a dream rate.

And if you’re already a homeowner? Don’t panic if your fixed rate ends and you’re offered 6.2%. Lock in a longer term. Build equity. Pay down extra. Small steps now make a huge difference later.

Final thought: It’s not about the rate - it’s about the plan

Mortgage rates aren’t magic numbers. They’re reflections of the economy - inflation, employment, global trade, and central bank confidence. The 3% rate was a flash in the pan. It won’t come back.

But that doesn’t mean homeownership is out of reach. It just means you need to plan differently. Focus on what you can control: your deposit, your income, your budget, and your long-term goals. Rates will move. Your strategy shouldn’t.

The next time you hear someone say, “I’m waiting for 3%,” ask them: “What are you willing to pay to get there?” Chances are, the price is higher than you think.