When you’ve spent decades saving for retirement, the last thing you want is a surprise tax bill when your pension payments start. The simple answer is: pensions are often taxed, but not always - and how much depends on where you live, how you took your money out, and what type of pension you have. In New Zealand, the rules are different from places like the U.S. or the U.K., and that’s where things get confusing.

What counts as a pension in New Zealand?

In New Zealand, most people don’t have private pensions like in other countries. Instead, they rely on Superannuation - the government-funded payment you get when you turn 65. This isn’t a pension you paid into over your working life. It’s a universal benefit, paid to most residents regardless of how much they saved. If you’ve lived in New Zealand for at least 10 years since turning 20, and five of those years after turning 50, you qualify.

Superannuation is not taxed. You get it tax-free, no matter your income level. That’s a big deal. It means your $500+ weekly payment from Work and Income doesn’t shrink because of income tax. No deductions. No forms to file. Just cash in your bank account.

But what if you have a private retirement fund? That’s where things change. Many Kiwis have KiwiSaver accounts - workplace or personal savings plans that help you save for retirement. When you withdraw from KiwiSaver at 65, the money you took out is also tax-free. That includes your own contributions, employer contributions, and government kick-starts. The growth inside the fund? Also tax-free.

When does retirement income get taxed?

Here’s the catch: if you’re still working past 65 and drawing from a private retirement fund like a superannuation fund or portfolio investment entity (PIE), the tax rules apply differently. These aren’t government pensions - they’re investment accounts.

For example, if you’re 70 and still taking regular payments from a PIE you set up during your working years, the income you get from those investments is taxable. The fund itself pays tax on earnings (like dividends or interest) at a flat rate based on your prescribed investor rate (PIR). But you don’t pay tax again on the money you withdraw. That’s called a “taxed fund” - the tax is already handled inside the fund.

On the other hand, if you invested in a non-PIE investment - say, rental properties or shares held directly - and you’re now selling assets to fund your retirement, you might owe tax. Capital gains aren’t taxed in New Zealand unless you’re a property speculator (buying and selling homes frequently). But if you’re taking dividends from shares, those are taxed as income.

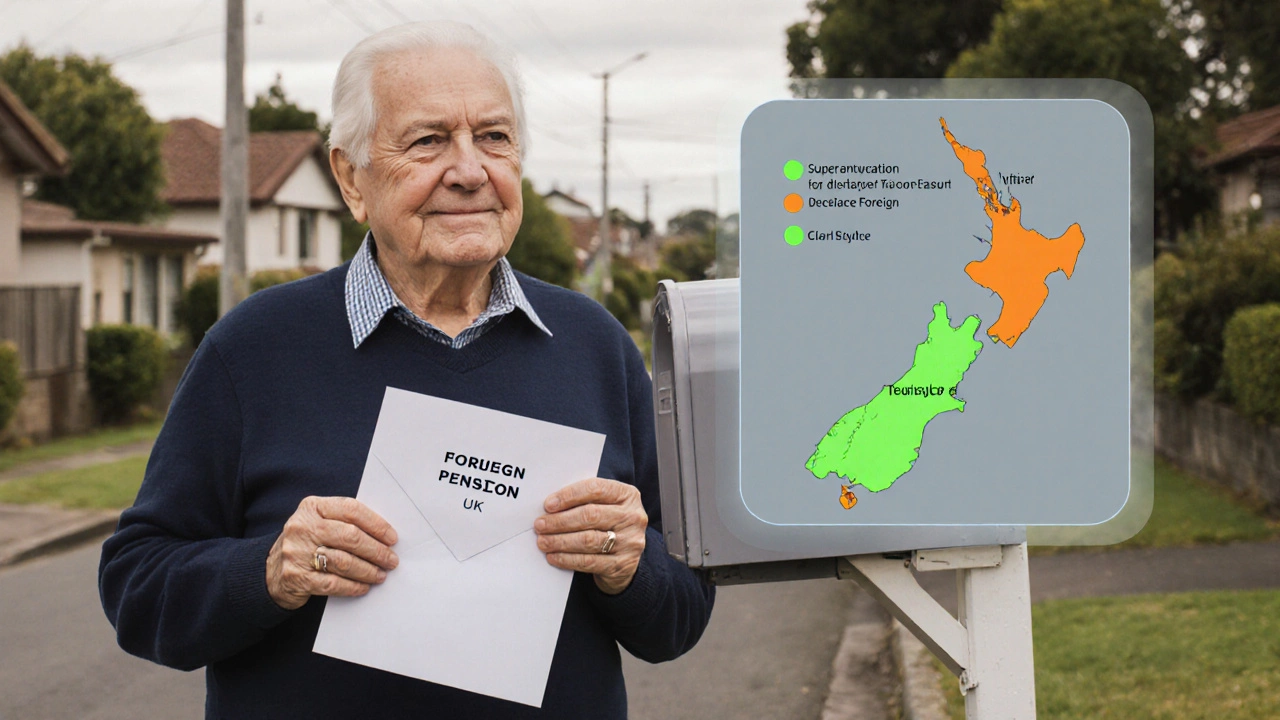

Foreign pensions and New Zealand tax

Many Kiwis retired abroad or worked overseas. If you’re getting a pension from the U.K., Australia, or the U.S., New Zealand doesn’t tax it - as long as you’re a resident here. But there’s a twist: your foreign pension might be taxed in the country you got it from. For example, the U.K. taxes its state pension if you live overseas, unless you’re in a country with a tax treaty. New Zealand doesn’t double-tax you, but you still need to declare foreign income if you’re a tax resident.

Some people forget they’re still tax residents in New Zealand even if they live overseas. If you own a home here, have family here, or return regularly, Inland Revenue might consider you a resident. That means you must declare all global income - including foreign pensions - on your New Zealand tax return.

What about lump sums?

Some people choose to take a big chunk of their retirement savings all at once. If you’re withdrawing from KiwiSaver at 65, you can take the whole amount as a lump sum - and still pay zero tax. Same goes for most superannuation funds. But if you’re taking a lump sum from a foreign pension, it’s different. The U.S., for example, may withhold 30% tax on lump sums paid to non-residents. New Zealand won’t tax it again, but you might need to claim a foreign tax credit if you file a return.

Don’t assume a lump sum is always better. Taking a large amount in one year could push you into a higher tax bracket for other income - like rental income or part-time work. It’s rarely the smartest move unless you need the cash for a specific purpose, like paying off debt or helping family.

Common mistakes people make

People assume all retirement money is tax-free. That’s not true. Only government Superannuation and KiwiSaver withdrawals are. Other sources? Not always.

- Thinking your overseas pension is tax-free in New Zealand - it’s not taxed here, but you still need to declare it.

- Withdrawing from a non-PIE investment fund and not tracking the tax already paid - you might owe more than you think.

- Delaying KiwiSaver withdrawals to avoid “tax” - but there’s no tax to avoid.

- Assuming tax rules from Australia or the U.K. apply here - they don’t.

One real case: A couple in Hamilton retired in 2024. They had $400,000 in KiwiSaver and $200,000 in shares. They took the KiwiSaver as a lump sum - tax-free. Then they sold shares worth $150,000. Because they held them for over two years and weren’t property traders, no capital gains tax applied. But the dividends they received from remaining shares? Those were taxed as income. They didn’t realize dividends counted as income - and got a surprise tax bill in April.

How to plan ahead

You don’t need a financial advisor to get this right. Just know the rules.

- Superannuation? Tax-free. Always.

- KiwiSaver? Tax-free when you withdraw at 65.

- Private superannuation funds? Tax is handled inside - you don’t pay again.

- Shares or property? Dividends and rental income are taxable. Capital gains usually aren’t.

- Foreign pension? Declare it if you’re a New Zealand tax resident.

If you’re still working part-time after 65, your pension payments won’t affect your income tax unless you’re earning over $14,000 a year. Superannuation doesn’t count toward that threshold. So you can earn $10,000 from a part-time job and still get your full $500+ weekly Superannuation - and pay no extra tax.

What’s changing in 2025?

As of 2025, there are no major changes to how pensions are taxed in New Zealand. Superannuation stays tax-free. KiwiSaver withdrawals remain tax-free. The government hasn’t touched the rules - and there’s no sign they plan to. Some politicians have floated ideas about taxing retirement savings, but nothing has passed. The system is stable for now.

What’s changing is awareness. More people are retiring with mixed income sources - KiwiSaver, property, shares, and part-time work. Understanding what’s taxed and what isn’t helps you avoid mistakes that cost thousands.

What if I’m under 65 and need money?

If you’re under 65 and withdrawing from KiwiSaver early - say, for a first home or serious illness - the rules are different. You don’t pay tax on the withdrawal, but you might lose the government contributions or employer matches. And if you’re taking money from a private retirement fund before 65, you might face penalties or tax. Always check with your provider.

There’s no penalty for early withdrawal from KiwiSaver for eligible reasons - but it’s not a loan. Once you take it out, you can’t put it back. Think long-term.

Final checklist: Are you taxed on your pension?

- Are you getting New Zealand Superannuation? → Not taxed

- Are you withdrawing from KiwiSaver at 65? → Not taxed

- Are you getting dividends from shares? → Taxed as income

- Are you renting out property? → Rental income taxed

- Are you receiving a foreign pension? → Declare it if you’re a NZ tax resident

- Are you withdrawing from a private super fund? → Tax already paid inside - no extra tax

If you answered yes to only the first two, you’re likely paying zero tax on your retirement income. That’s the norm in New Zealand. Most people don’t pay tax on their pension - because their pension is Superannuation, and it’s designed to be tax-free.

Is New Zealand Superannuation taxed?

No, New Zealand Superannuation is not taxed. It’s paid to you tax-free, regardless of your other income. You don’t need to file a tax return for it, and no deductions are made.

Are KiwiSaver withdrawals taxed at 65?

No. When you withdraw from KiwiSaver at age 65, all your contributions, employer contributions, and investment growth come out tax-free. This includes lump sums and regular payments.

Do I pay tax on foreign pensions in New Zealand?

New Zealand doesn’t tax foreign pensions if you’re a tax resident here. But you must declare them on your tax return. The country that pays the pension might withhold tax - like the U.S. or U.K. - but New Zealand won’t tax it again.

Is retirement income from shares taxed?

Dividends from shares are taxed as income. Capital gains from selling shares are usually not taxed unless you’re trading frequently. If you’re holding shares for long-term income, you pay tax on the dividends, not the sale.

Can I avoid tax by taking my pension as a lump sum?

If it’s from KiwiSaver or Superannuation, taking a lump sum doesn’t change anything - it’s still tax-free. But if you’re selling investments to create a lump sum, you might trigger tax on dividends or capital gains. A lump sum doesn’t magically avoid tax - it just changes when you pay it.