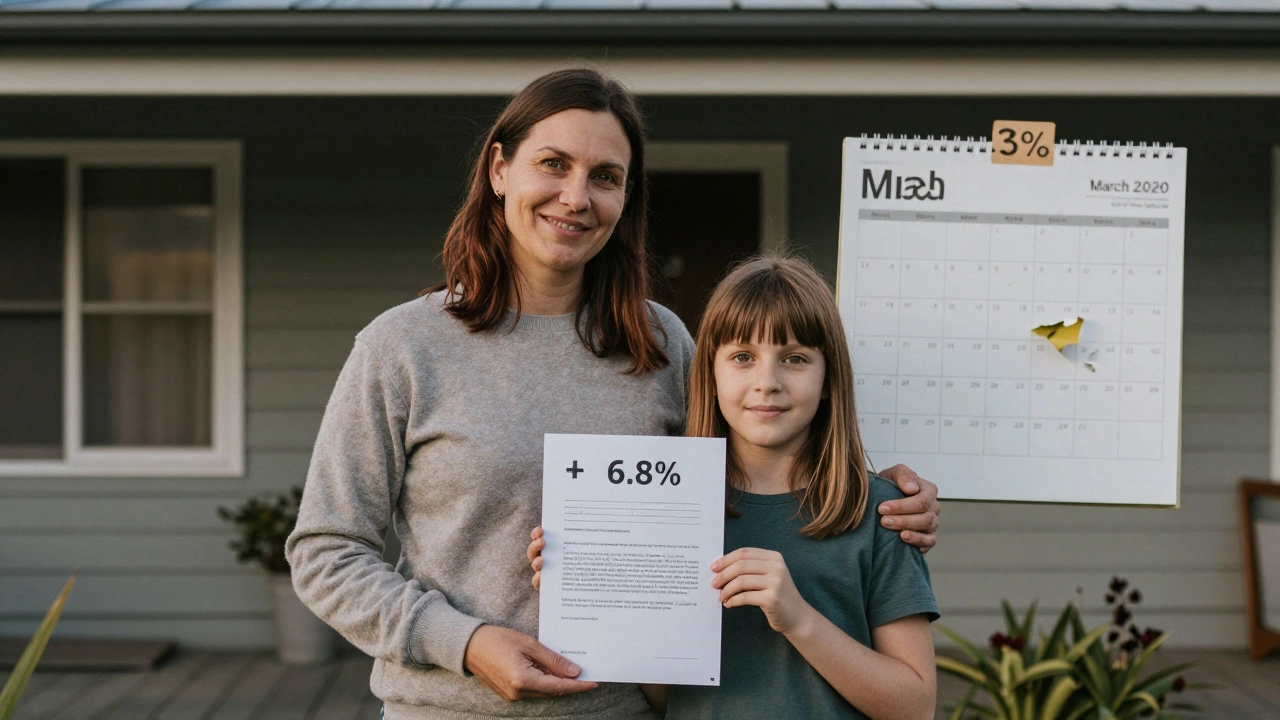

Will mortgage rates ever be 3% again?

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

Looking for a mortgage can feel like stepping into a maze. You want a loan that fits your budget, lets you borrow enough, and won’t trap you with hidden fees. This guide cuts the jargon and gives you straight‑forward steps to pick, manage and improve your home loan.

First, check your credit score. A higher score usually means a lower interest rate, which saves you money over the life of the loan. If your score is low, consider fixing errors on your report before you apply.

Next, compare the type of interest rate. Fixed rates stay the same, so your monthly payment won’t change. Variable rates can drop when the market eases, but they can also rise. Decide which feels safer for your budget.

Don’t forget to look at the loan‑to‑value (LTV) ratio. Lenders often let you borrow up to 80‑90% of the property’s value. If you can put down a bigger deposit, you’ll get a lower LTV and better terms.

Use an online calculator to see how different rates and terms affect your payment. Switch a 30‑year term to 25 years and you’ll pay less interest, even though the monthly amount goes up a bit.

Once you’re settled, keep an eye on refinancing options. If rates drop by 0.5% or more, a refinance could shave a few hundred pounds off your annual payment. Make sure the savings cover any break‑fees or legal costs.

Equity release is another route if you’re over 55 and own your home outright. You can tap the value of your house without monthly repayments, but the interest compounds daily. Read the fine print and use a calculator to see the long‑term cost.

If you need extra cash but don’t want to remortgage, a home‑equity loan or HELOC (home equity line of credit) might be cheaper. These let you borrow against the equity you’ve built, usually at a lower rate than a personal loan.

Remember to budget for insurance and taxes. Missing a payment can damage your credit score and trigger penalties that hurt your loan balance.

Finally, track your mortgage balance each year. Seeing the principal shrink can motivate you to make extra payments when you get a bonus or tax refund. Even a small lump sum can cut years off your loan.

Home loans don’t have to be a mystery. By checking your credit, comparing rates, and staying aware of refinancing or equity‑release options, you keep control of your finances and protect your home for the long run.

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

Ever wondered if switching your mortgage is less hassle than applying for a new one? This article compares the remortgaging process with getting a new mortgage, breaking down the steps, paperwork, and hidden hurdles. Find out where the biggest time-savers are, what catches homeowners off guard, and tips that save you nerves and money. Whether you're hunting for better rates, more flexible terms, or just curious about the whole thing, you'll get clear answers. No jargon, just honest advice about how this really plays out.

Remortgaging can be a beneficial financial move, but it's not without its pitfalls. Without careful consideration, you might find yourself facing higher costs or losing favorable terms. This article delves into potential risks like increased interest rates and hidden fees while offering practical tips on making informed decisions during the remortgaging process to safeguard your financial health.