Will mortgage rates ever be 3% again?

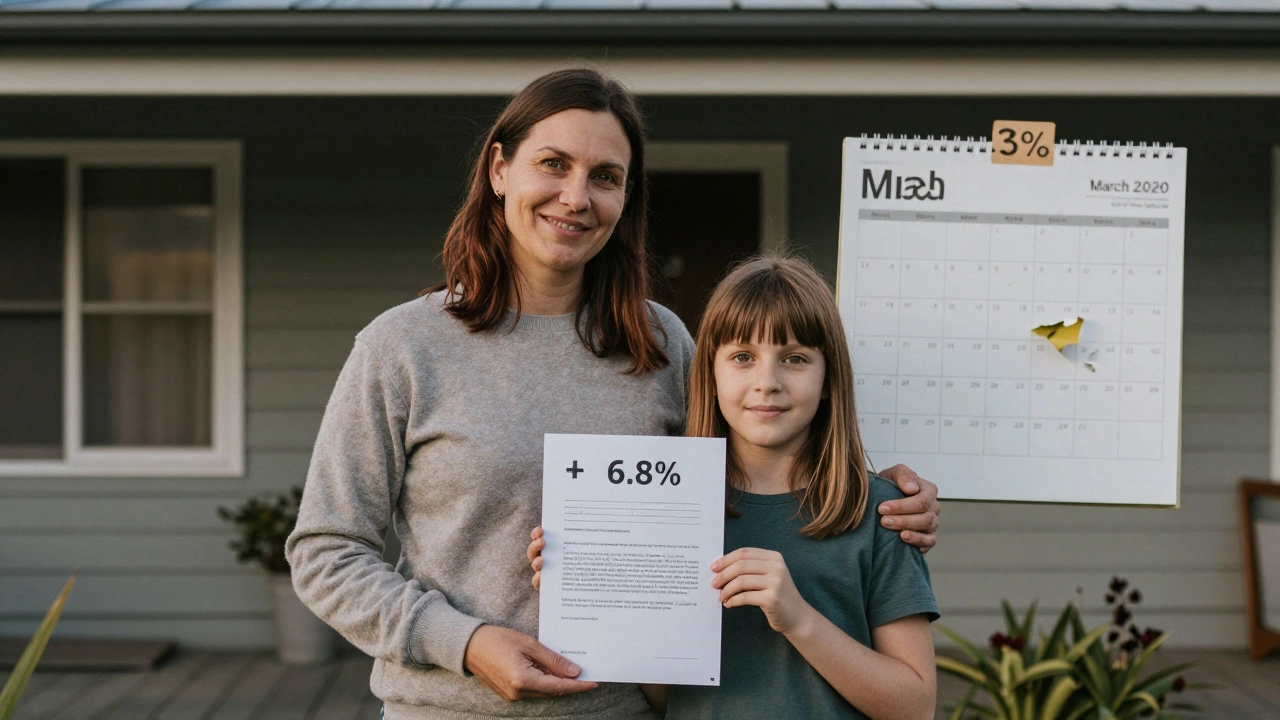

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

Interest rates show up everywhere – on your credit card, mortgage, personal loan and even your savings account. When the rate goes up, your monthly bill rises. When it drops, you pay less. Understanding why rates move and how to react can save you a lot of money.

Think of an interest rate as the cost of borrowing money. If you swipe a credit card and don’t pay the full balance, the bank adds a percentage to what you owe. That percentage is the interest rate. For a mortgage, the rate decides how much of each payment goes toward the loan versus the interest. A higher rate means more of your money goes to interest and less to the actual loan.

In the UK, the Bank of England sets the base rate. Banks use that number to figure out what they’ll charge you. When the base rate shifts, most lenders follow quickly. That’s why you’ll hear news about the Bank of England raising or cutting rates – it’s a signal that your credit‑card bill, mortgage payment, or loan might change soon.

1. Check the APR, not just the headline rate. APR (Annual Percentage Rate) includes fees and tells you the real cost over a year. Two cards might show 18% and 20% headline rates, but the APR could be closer together.

2. Look for introductory offers. Some cards give 0% for the first 12 months. That can be handy for paying off a big purchase, but make sure you know what the rate will be after the intro period.

3. Compare fixed vs variable rates. Fixed rates stay the same for the agreed period – good if you want certainty. Variable rates move with the base rate, which can be lower now but might rise later.

4. Read the fine print on mortgage deals. Many lenders advertise a low “teaser” rate for the first two years, then jump to a higher rate. Calculate the total cost over the whole mortgage term before you decide.

5. Use rate comparison tools. Websites that list current credit‑card and mortgage rates let you sort by APR, balance transfer fee, or rewards. It’s faster than calling each bank.

6. Negotiate. If you’ve been a good customer, ask your bank for a better rate. Sometimes a quick call can shave a few points off your mortgage or loan.

7. Watch the news. When the Bank of England hints at a change, lock in a rate early. A small move in the base rate can add up to hundreds of pounds over a loan’s life.

Lastly, remember that the lowest rate isn’t always the best choice. A card with a low rate but a high annual fee could cost more in the long run. Balance the rate with fees, rewards, and how you plan to use the product.

By keeping an eye on the base rate, checking APR, and comparing offers, you can stay ahead of interest‑rate changes and keep more of your money where it belongs – in your pocket.

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

Thinking about equity release? Find out exactly how much you repay, how interest works, and see up-to-date examples for 2025.

Cut through the myths: do ISAs actually lose money in 2025? Get real answers, smart strategies, and fresh data to make your savings work harder.

Wondering what the monthly payments look like for a $150,000 mortgage? This article breaks down the numbers with current rates, explains why the term you choose matters, and shares ways to lower your bill. You'll find relatable examples, real-world tips, and quick answers to big questions so you don't get tripped up by small print. Get the info you need up front to figure out your next move.

Savings accounts have traditionally been seen as a safe place to park your money, but are they costing you money in the current economy? With low interest rates, inflation, and other investment opportunities, it’s crucial to weigh the pros and cons. Learn how your savings account might not be keeping up with inflation and explore alternatives for potentially higher returns. Making informed decisions could help protect your financial future.