Is it better to remortgage with an existing lender?

Staying with your current lender when remortgaging can save you thousands in fees and time. Learn when to stick with them-and when to switch-for the best deal on your home loan.

Looking at a mortgage can feel like stepping into a maze. What matters most is understanding the basics, so you can avoid costly mistakes. Below you’ll find quick answers, real examples, and practical tips that cut through the jargon.

Remortgaging is simply swapping your current mortgage for a new deal. It can lower your interest rate, free up cash, or change the loan term. Think of it like switching to a cheaper mobile plan – you keep the same phone (your house) but pay less each month.

Most people wonder how often they can remortgage. There’s no hard limit, but each switch brings fees and a credit check. If you’re planning to move again soon, the extra cost might outweigh the savings. Use a calculator to compare your current monthly payment with the new one before you decide.

Timing is key. Interest rates fluctuate, and a lower rate can shave hundreds off your yearly bill. Pay attention to the “break fee” – the charge for leaving your current deal early. If the fee is smaller than the long‑term savings, a switch makes sense.

Want to pay less each month? Start by checking if a shorter loan term reduces your interest rate. Yes, the monthly amount goes up, but you pay off the loan faster and save on total interest.

Another option is a top‑up loan. You borrow extra money against the equity you’ve built, without a full remortgage. It can be handy for home improvements or consolidating debt, but keep an eye on the new interest rate.Refinancing in the US is called “refi”; in the UK, it’s often called “remortgaging”. Both do the same thing – replace the old loan with a new one. The impact on your credit score is usually small, especially if you shop around with one lender at a time.

Watch out for hidden costs. Some lenders add admin fees, valuation charges, or higher arrangement fees. Write down every expense before you sign, then subtract it from the total savings you expect.

Finally, keep your credit score healthy. Pay all bills on time, reduce credit card balances, and avoid opening new accounts right before you apply. A good score gives you more negotiating power and better rates.

Whether you’re buying your first home, thinking about a second mortgage, or just curious about how many times you can switch deals, the right information saves you money and stress. Use the articles below for deeper dives – from real‑world payment examples to step‑by‑step guides on working with a new lender.

Staying with your current lender when remortgaging can save you thousands in fees and time. Learn when to stick with them-and when to switch-for the best deal on your home loan.

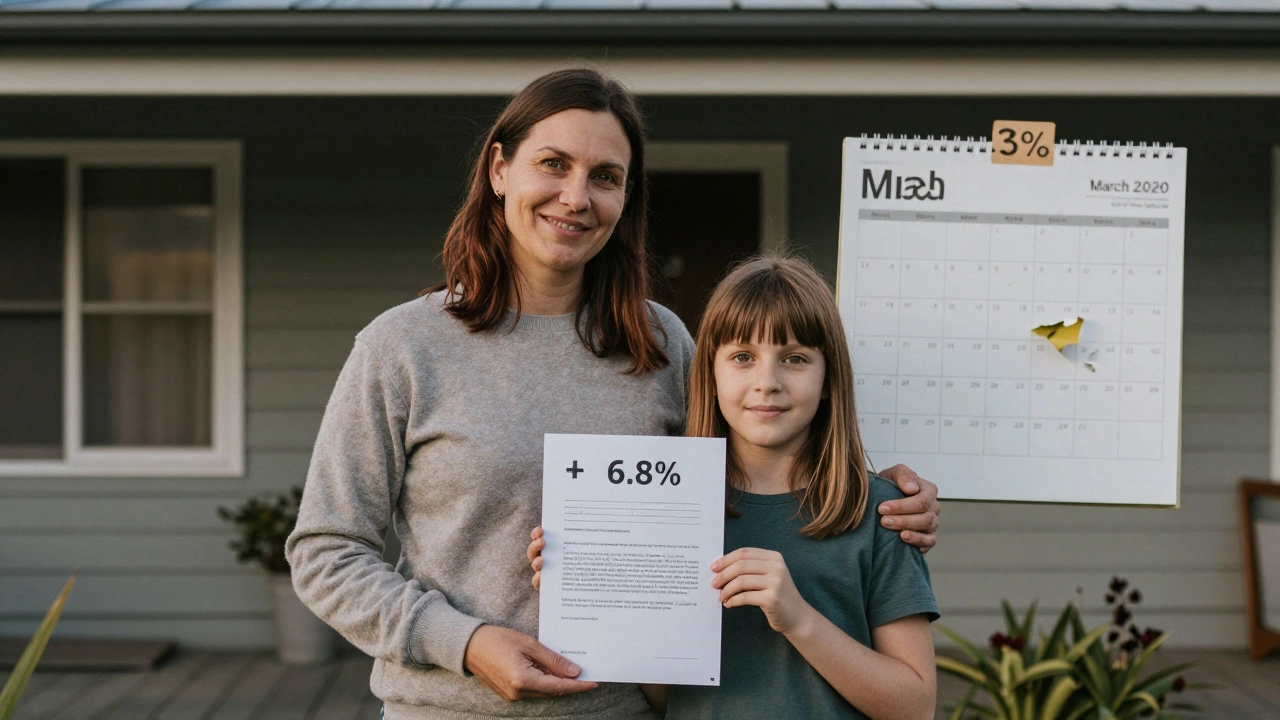

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

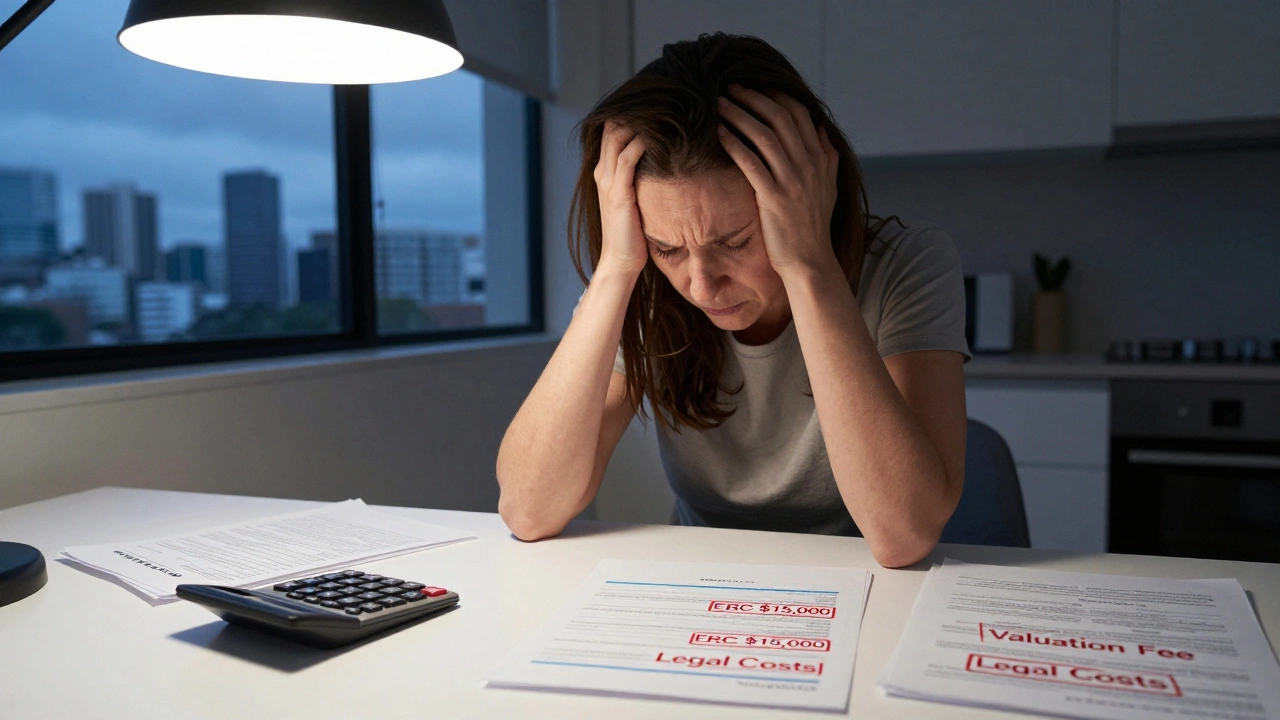

Remortgaging can save money - or cost you tens of thousands. Learn the real risks in New Zealand: hidden fees, extended terms, equity traps, and credit score damage. Know when it's smart - and when to walk away.

Remortgaging can save money, but hidden fees, credit hits, extended loan terms, and rate resets often make it cost more in the long run. Know the risks before you switch in New Zealand in 2025.

Discover how to lock in the lowest mortgage rates in New Zealand for 2025. Compare major banks, learn key factors, and follow a step‑by‑step plan to secure the best deal.

Explore whether a HELOC makes sense in 2025, covering its definition, current rates, pros, cons, alternatives, qualification tips, and step‑by‑step application guidance.

Will remortgaging lower your repayments? Learn when payments fall or rise in NZ, the math, fees, and steps. Clear examples, checklists, and risks to avoid.

Wondering if refinancing hurts your credit? Discover how mortgage refinance actually affects credit scores, what to expect, and tips to protect your score.

Curious what a $100k mortgage over 15 years costs? Get insights into repayments, real numbers, interest tips, and smart ways to pay less in New Zealand.

Thinking about raising cash without remortgaging? Discover practical ways to borrow more on your mortgage, the pros, cons, and what to watch out for.

Ever wondered if switching your mortgage is less hassle than applying for a new one? This article compares the remortgaging process with getting a new mortgage, breaking down the steps, paperwork, and hidden hurdles. Find out where the biggest time-savers are, what catches homeowners off guard, and tips that save you nerves and money. Whether you're hunting for better rates, more flexible terms, or just curious about the whole thing, you'll get clear answers. No jargon, just honest advice about how this really plays out.

Wondering what the monthly payments look like for a $150,000 mortgage? This article breaks down the numbers with current rates, explains why the term you choose matters, and shares ways to lower your bill. You'll find relatable examples, real-world tips, and quick answers to big questions so you don't get tripped up by small print. Get the info you need up front to figure out your next move.