What Are Examples of Not Covered Homeowners Insurance Situations?

Discover common exclusions in home policies including floods, pests, and mold. Learn which gaps to fill with additional riders or separate policies.

Discover common exclusions in home policies including floods, pests, and mold. Learn which gaps to fill with additional riders or separate policies.

Understand the most basic homeowners insurance policy options, including HO-3 and HO-8 forms, coverage limits, and valuation methods.

Discover how much equity you can actually release from your home in 2026. Learn the factors setting your limit, including age, property type, and loan options.

A pension plan is a structured way to save for retirement through regular contributions, employer matches, and long-term investing. In New Zealand, KiwiSaver is the most common form, helping millions build secure retirements.

Leftover budget isn't just extra cash - it's unallocated funds. Learn how naming it changes your financial habits, avoids impulse spending, and helps you build real wealth with zero-based budgeting.

Staying with your current lender when remortgaging can save you thousands in fees and time. Learn when to stick with them-and when to switch-for the best deal on your home loan.

In 2026, you can get 8% interest on savings in New Zealand through fixed-term deposits from regulated institutions - but only if you lock away your money for 12-24 months. Learn where to find these offers, what conditions apply, and how to avoid scams.

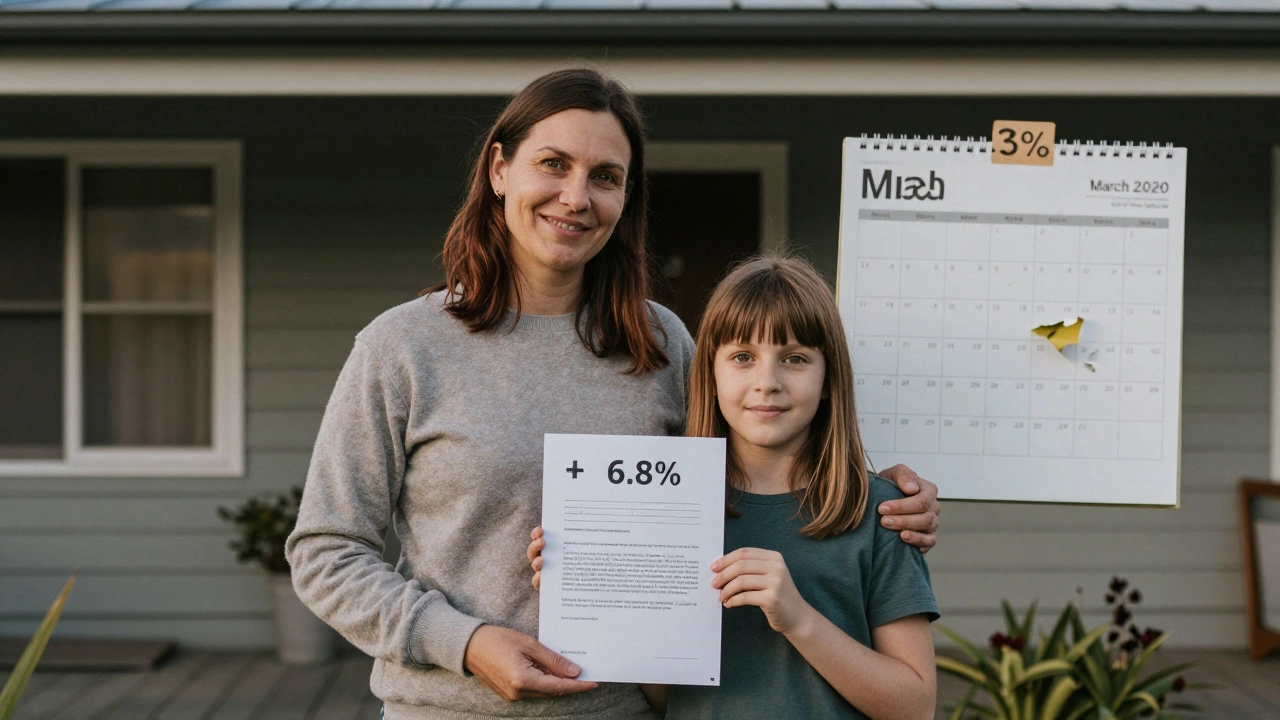

Mortgage rates in New Zealand are near 7% in 2026. Will they ever return to 3%? History, economics, and market trends suggest it's highly unlikely - and waiting for it could cost you more than you save.

No UK bank offers 7% interest on savings accounts, but top rates are hitting 6.25% through fixed-term ISAs. Learn where to find the safest, highest-paying accounts in 2026 - and how to avoid scams.

In 2026, $1000 in a standard savings account earns just $18, but switching to a high-yield account can earn you over $50. Learn how interest rates, compounding, and account types affect your returns-and what to do right now.

In 2026, three New Zealand banks are offering savings accounts with interest rates near 7%. Learn who they are, what the requirements are, and how to qualify without risking your money.

Closing a credit card with a zero balance might seem smart, but it can hurt your credit score. Learn why keeping it open - even unused - often helps more than closing it.